The technological and organisational transition from network operator to Digital Service Provider (DSP) is no laughing matter. It comes with a fairly long roadmap, complex integrations, and in some cases, paradigm shifts in the way business is done.

As the industry looks at the current state of digital transformation across the globe, the predominant signs are that operators are moving slowly. The lack of urgency may be seen as a negative, but it is important to note that there is good news amidst the negative chatter. As Aesop said in his famous fable “The Tortoise and the Hare,” the moral of the story is “Slow and steady wins the race”, says Paul Hughes, director of strategy, Netcracker Technology

The telecommunications industry is in the midst of network transformation, with significant time and money invested in global infrastructure and systems to enable greater levels of virtualisation and enhanced flexibility of service offers and bundles. For many, that includes the complete replacement of an existing, interoperable global network architecture with IP, LTE, 5G, and/or fiber, based on the prior technology already in place.

This transition must be completed without any interruptions to existing services, which is of course dependent on legacy processes and business models. As a result, today’s operators are rightly cautious in pursuing a two-speed architectural roadmap that allows for business continuity at the same time IT is undergoing a metamorphosis to complement the network upgrades.

A successful DSP strategy should enable newfound agility to address market changes, greater proactivity around customer needs, and ensuring a rich customer experience across increasingly complex product and service lines without upsetting day-to-day operations.

It begs the question: Is the industry making enough progress along the DSP path?

A recent 2017 DSP survey from analyst firm ICT intuition, which follows up on a previous year’s survey, shows that while some geographic regions are showing slower signs than others, the general trend towards digital remains positive. 79% of operators either have a completely defined DSP strategy or are in progress. Currently, 33% of all operators interviewed stated that their DSP strategy is fully implemented. In its entirety, the roadmap for DSPs is tied to three key areas; the network, the service delivery and modernisation of the customer interaction.

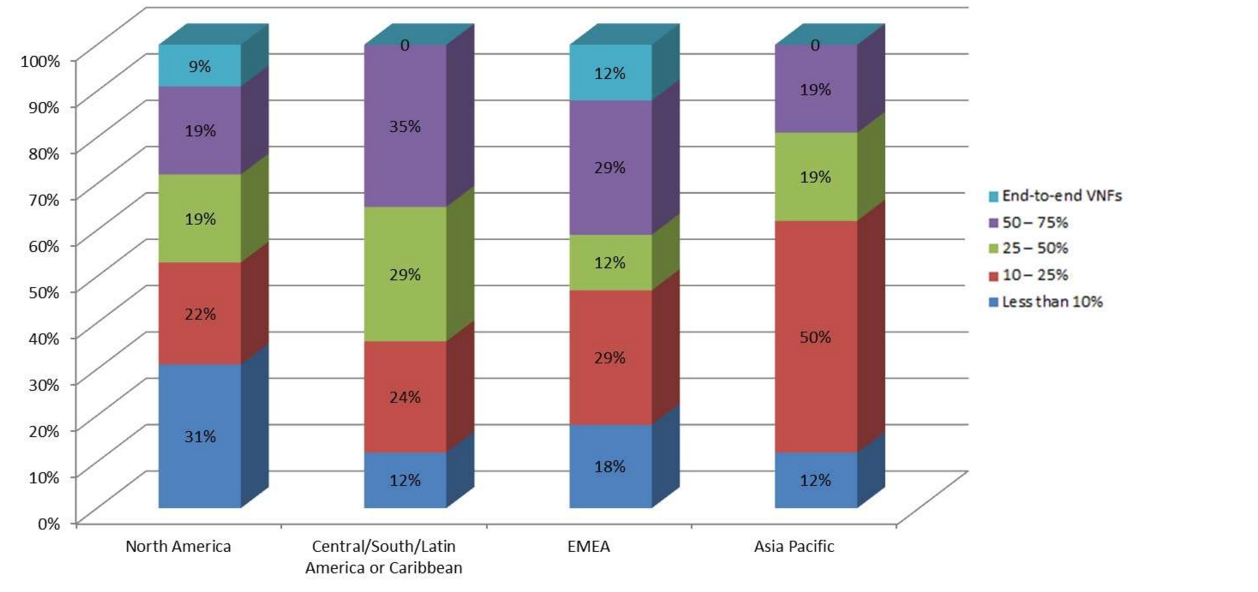

Figure 1: Percentage of Network Virtualisation by Geographic Region

The network

Implementing digital network technology remains the operator’s biggest challenge. Through the investment on the network, operators have been focused on transforming trillions of dollars’ worth of global interconnected infrastructure with the hopes of revenue payback from the broader capabilities. Today, the breakdown of network virtualisation rates by operator in different regions shows surprisingly faster timelines by carriers in LATAM and EMEA as shown in Figure 1.

Source: ICT intuition

While this may come as a surprise, it’s important to remember that the network transformation timeframe is intrinsically linked to the scale and complexity of the network itself. For operators in North America, past consolidation of networks, geographic scale, and a business outcome minded approach contribute to the slower path to virtualisation. Notwithstanding the scale issue, it is important to note that North America and EMEA are the two regions with operators that have actually achieved virtualisation to the point where Virtual Network Functions are available today.

Service delivery

Delivering digital services is taking longer than expected, but it’s moving in the right direction. In the first survey, CSPs remained focused on delivering network services, and while new services aren’t coming to market as fast as they would like, there are some bright spots. Ultimately, the benefits of becoming a DSP will revolve around the ability to roll out a wide variety of new services rapidly, monetise those services, and establish automated partner platforms. DSPs need to put themselves in positions to broker access to a wide variety of partners that will come and go based on demand, economics, or geography.

Currently more than 85% of the operators surveyed take one month or more to launch a new service, pricing plan, or product bundle. While that is considered progress by operators that regularly required six months or more to bring a new service to market, the ability to respond rapidly to customer demand with unique, customised products and offers is a big part of being able to monetise expensive digital infrastructure and needs to happen even faster.

The author of this blog is Paul Hughes, director of strategy, Netcracker Technology

Comment on this article below or via Twitter: @ VanillaPlus OR @jcvplus